Topic how much can california property taxes increase: California property taxes are subject to strict regulations and limits under the state\'s Constitution, specifically Proposition 13. This landmark amendment ensures that property taxes can only increase by a maximum of 2% per year, which provides stability and predictability for homeowners. This safeguard protects individuals from experiencing drastic and unaffordable hikes in property taxes, allowing them to plan their expenses and secure their homes without undue burden.

Table of Content

- How much can California property taxes increase?

- What is Proposition 13 in California and how does it affect property taxes?

- What is the maximum annual increase allowed for property taxes in California?

- YOUTUBE: ADU Property Tax Impact in California

- How is the factored base year value determined for properties in California?

- Are there any exceptions to the 2% annual increase limit for property taxes in California?

- Can property taxes increase more than 2% in a single year under certain circumstances?

- How are property tax rates calculated in California?

- What factors can lead to an increase in property taxes in California?

- Are there any steps homeowners can take to lower their property tax bills in California?

- How does the taxpayers\' collective response to property tax increases and state revenue surplus play a role in California\'s property tax system? Remember, these questions are meant to form the basis for an in-depth article on the topic.

How much can California property taxes increase?

In California, property taxes are governed by Proposition 13, which places a limit on the amount property taxes can increase each year. Under Proposition 13, property taxes can only increase a maximum of 2% per year. This is known as the \"2% cap\" or \"2% increase per year.\"

The starting point for property tax calculations is the factored base year value, which is typically the property\'s value at the time of purchase. Once the factored base year value is established, the property tax can increase by a maximum of 2% per year.

It\'s important to note that the 2% cap applies to the assessed value of the property, which is usually lower than the market value. The assessed value is determined by taking the factored base year value and then adjusting it based on changes in the real estate market and the cost of living.

While the 2% cap provides some stability and predictability for property owners, it\'s worth noting that there are certain circumstances that can result in larger increases in property taxes. For example, if the property undergoes substantial improvements or changes in ownership, the assessed value can be reassessed and potentially result in a larger increase in property taxes.

Overall, the maximum increase in property taxes in California is 2% per year, but it\'s important to monitor any potential changes in property value or ownership that could impact the assessed value and ultimately the property tax amount.

READ MORE:

What is Proposition 13 in California and how does it affect property taxes?

Proposition 13 is a California state law that was enacted in 1978. It has significant implications for property taxes in the state. Here\'s how it works:

1. Property Valuation: Proposition 13 set a system for property valuation. It established the base year value, which is determined as the property\'s value in 1975, with limited adjustments for inflation. This value serves as the starting point for calculating property taxes.

2. Tax Limitations: Proposition 13 introduced a tax limitation on property assessments. It limited the annual increase in assessed value to a maximum of 2% unless there is a change in ownership or substantial improvement to the property.

3. Tax Rate: Proposition 13 also establishes a maximum tax rate of 1% of the property\'s assessed value. This means that the property tax paid by a homeowner is generally 1% of their property value at the time of purchase, plus any additional voter-approved taxes or fees.

4. Reassessment: Under Proposition 13, a property is reassessed only when it changes ownership or undergoes significant improvements. This means that even if the market value of a property increases, the property taxes are not adjusted until the property is sold or remodeled.

The implications of Proposition 13 are that property taxes in California tend to be relatively stable and predictable for homeowners. The tax rate is kept at a maximum of 1%, and the annual increases in assessed value are limited to a maximum of 2% for properties that have not changed ownership or undergone substantial improvements.

However, it is important to note that Proposition 13 can also lead to disparities in property tax burdens. Properties that have not recently changed ownership can accumulate significant differences between their assessed value and their market value, leading to disparities in property tax payments between long-time homeowners and newer buyers.

In summary, Proposition 13 in California is a law that sets limitations on property taxes, including a maximum annual increase in assessed value and a maximum tax rate. It provides stability for homeowners but can also lead to disparities in tax burdens.

What is the maximum annual increase allowed for property taxes in California?

The maximum annual increase allowed for property taxes in California is 2%. This is based on Proposition 13, which was passed in 1978. According to Proposition 13, property taxes can only increase by a maximum of 2% per year. This limitation applies to the factored base year value, which is the assessed value of a property as of the time it was acquired, with adjustments for inflation. So, regardless of any increase in the property\'s market value, the property taxes can only go up by a maximum of 2% each year. This measure was introduced to protect homeowners from skyrocketing property tax increases, especially during periods of rapid appreciation in real estate values.

ADU Property Tax Impact in California

Discover the potential impact of ADU property taxes in California and stay informed about the recent property tax increase. Watch this video to gain valuable insights and understand how it may affect your property taxes.

Understanding Property Taxes: A Comprehensive Guide

Are you struggling to understand property taxes? Look no further! This comprehensive guide has got you covered. Watch this video to receive a comprehensive overview of property taxes and become knowledgeable on the topic.

How is the factored base year value determined for properties in California?

The factored base year value for properties in California is determined based on a system of property taxation known as Proposition 13. This system values the property at its 1975-1976 market value, which is known as the base year value.

The base year value is then factored each year to determine the assessed value for property tax purposes. The factoring is done based on the lesser of both market value inflation and a 2% increase per year. This means that the assessed value cannot increase more than 2% annually, even if the market value increases at a higher rate.

To calculate the factored base year value, you would start with the base year value of the property and apply the appropriate factors for each year. For example, if a property has a base year value of $200,000 and has been owned for 10 years, the factored base year value would be calculated as:

Year 1: $200,000 (base year value)

Year 2: $200,000 + 2% = $204,000

Year 3: $204,000 + 2% = $208,080

...

Year 10: $228,784 + 2% = $231,559.68 (factored base year value)

It\'s important to note that there are some exceptions and additional rules for properties that have undergone certain changes, such as changes in ownership or new construction. These changes may trigger a reassessment and potentially a different method for determining the factored base year value.

Overall, the factored base year value determines the assessed value of a property for property tax purposes in California, and it is calculated based on the base year value and annual factors, subject to certain limitations and exceptions outlined in Proposition 13.

Are there any exceptions to the 2% annual increase limit for property taxes in California?

Yes, there are exceptions to the 2% annual increase limit for property taxes in California. Proposition 13, which is the state\'s system of property taxation, allows for certain circumstances in which property taxes can increase beyond the 2% limit. The following are some exceptions:

1. New Construction: When a new building or structure is constructed, its assessed value is determined based on the market value at the time of completion. This means that the property taxes for the new construction will not be limited by the 2% increase cap.

2. Change in Ownership: When a property changes ownership, its assessed value is adjusted to reflect the current market value. The new assessed value can be higher than the previous assessed value, resulting in an increase in property taxes greater than 2%.

3. Significant Improvements: If substantial improvements or renovations are made to a property, its assessed value can be increased beyond the 2% limit. The increase will be based on the market value added by the improvements.

It is important to note that these exceptions apply to specific situations, and the 2% annual increase cap still generally applies to most properties in California. Property owners should consult with their local county assessor\'s office for specific information regarding their property tax assessments.

_HOOK_

Can property taxes increase more than 2% in a single year under certain circumstances?

Under certain circumstances, property taxes can increase more than 2% in a single year in California. However, this is subject to specific conditions outlined in Proposition 13. Proposition 13, which was adopted in 1978, limits property tax increases to a maximum of 2% per year for properties that have not undergone a change of ownership or new construction.

Here is a step-by-step breakdown:

1. Proposition 13: California\'s property taxation system is governed by Proposition 13, which bases property taxes on the property\'s assessed value at the time of purchase. This assessed value is known as the base year value.

2. Maximum 2% Increase: Proposition 13 caps the annual property tax increase at 2% for properties that have not experienced a change of ownership or been newly constructed. This means that property taxes can generally only increase by up to 2% per year for most properties.

3. Change of Ownership: If a property undergoes a change of ownership, the property\'s assessed value is reassessed to its current market value. At this point, the property\'s tax liability may increase significantly, as it is based on the new market value.

4. New Construction: Similarly, if a property undergoes new construction or substantial remodeling, the assessed value will be adjusted to reflect the enhancements. This can lead to a higher property tax assessment than the previous year.

5. Local Assessments and Bond Measures: In addition to the 2% cap, property taxes can also increase due to local assessments and voter-approved bond measures. These assessments and bonds are separate from the Proposition 13 limitations and can result in higher property tax bills.

In summary, while Proposition 13 sets a standard 2% cap on property tax increases each year, certain circumstances such as a change of ownership, new construction, local assessments, or bond measures can cause property taxes to increase more than the standard limit. It is important to consult with local tax authorities or a tax professional to understand the specific rules and regulations that apply to your property.

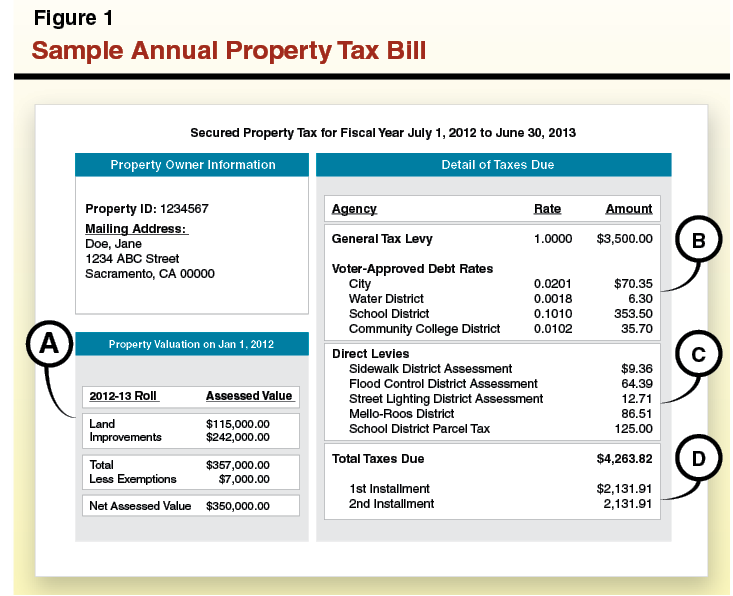

How are property tax rates calculated in California?

In California, property tax rates are calculated based on the assessed value of the property. The assessed value is determined by the county assessor and is generally based on the purchase price of the property plus any adjustments for market value changes.

Here\'s a step-by-step process on how property tax rates are calculated in California:

1. Determine the assessed value of the property: The county assessor assesses the value of the property based on its purchase price, generally using the most recent transaction as a starting point. This assessed value is the taxable value of the property.

2. Apply Proposition 13: California\'s Proposition 13 limits the increase in assessed value to a maximum of 2% per year. This means that the assessed value of the property can only increase by a maximum of 2% each year, even if the market value of the property has increased at a higher rate.

3. Calculate the taxable value: To determine the taxable value, the assessed value is multiplied by the property tax rate. In California, the property tax rate is generally set at 1% of the assessed value.

4. Consider additional taxes: In addition to the 1% property tax rate, there may be additional taxes levied on the property. These additional taxes could be for local school districts, bonds, or special assessments. These additional taxes are based on the assessed value of the property as well.

5. Calculate the total property tax amount: To calculate the total property tax amount for the year, the taxable value is multiplied by the property tax rate and any additional taxes applicable to the property.

It is important to note that there can be variations and exceptions to these general guidelines depending on specific circumstances, such as changes in ownership or new construction. Additionally, it\'s always recommended to consult with a tax professional or the local county assessor\'s office for specific information and details regarding property tax calculations in California.

What factors can lead to an increase in property taxes in California?

There are several factors that can lead to an increase in property taxes in California. Here are some of the main factors:

1. Market Value of the Property: Property taxes in California are based on the assessed value of the property, which is determined by the market value. If the market value of your property increases, it can result in an increase in property taxes.

2. Proposition 13: Proposition 13, which was passed in 1978, limits the increase in assessed value of a property to no more than 2% per year, unless there is a change in ownership or new construction. However, when there is a change in ownership or new construction, the assessed value can be adjusted to reflect the current market value, which can result in an increase in property taxes.

3. Local Tax Rates: Property tax rates can vary among different cities, counties, and special districts within California. If there is an increase in local tax rates, it can lead to an increase in property taxes.

4. Special Assessments: Some properties in California may be subject to special assessments, such as for local infrastructure improvements or community facilities. If a special assessment is imposed or increased, it can result in an increase in property taxes.

5. Changes in Tax Laws: Changes in tax laws or regulations at the state or local level can also impact property taxes. For example, the state legislature may pass laws that increase property tax rates or remove certain exemptions.

It\'s important to note that property tax increases in California are subject to certain limitations and protections, such as Proposition 13. However, there are still factors that can lead to an increase in property taxes based on the specific circumstances of the property and the local tax laws.

Exploring California Property Taxes: Key Factors to Consider

If you\'re planning to invest in California real estate, understanding the key factors that affect property taxes is essential. Tune into this video to explore the intricacies of California property taxes and empower yourself to make informed decisions.

Are there any steps homeowners can take to lower their property tax bills in California?

Yes, there are several steps that homeowners can take to potentially lower their property tax bills in California. Here is a step-by-step guide:

1. Understand Proposition 13: Proposition 13 is a California law that limits property tax increases. It values property at its 1975 assessed value and restricts annual increases to a maximum of 2% as long as the property is not sold or undergoes significant renovations. Knowing the limits set by Proposition 13 will help you assess your options.

2. Verify property assessment: Start by reviewing your property assessment to ensure its accuracy. Mistakes can happen, and if your property is assessed at a higher value than it should be, it could result in excessive property taxes. Contact your local assessor\'s office to request a review or correction if needed.

3. Understand exemptions and deductions: California offers various exemptions and deductions that can lower your property tax burden. For example, the Homeowners\' Exemption provides a modest reduction in assessed value for owner-occupied residences. Additionally, certain circumstances such as being a senior citizen or disabled may qualify you for additional exemptions or assessment discounts. Research and determine if you qualify for any exemptions or deductions available in your area.

4. Consider reassessment appeals: If you believe your property is over-assessed, you can file an appeal with your local assessment appeals board. This process allows you to present evidence supporting a lower valuation. Familiarize yourself with the appeal process in your county and gather all relevant evidence to support your case.

5. Utilize property tax reduction programs: California offers programs that assist low-income homeowners and seniors in reducing their property taxes. For example, the Property Tax Postponement (PTP) program defers property taxes for eligible homeowners who meet specific income requirements. Explore these programs to determine if you qualify for any assistance.

6. Monitor property improvements: Keep track of any renovations or improvements made to your property. While Proposition 13 limits annual reassessments, significant improvements can trigger a reassessment at market value. Understanding how property improvements impact your tax liability will help you plan accordingly.

7. Consult with a tax professional: If you are unsure about navigating the complexities of property taxation in California, it may be beneficial to consult with a tax professional or a real estate attorney. They can provide personalized advice based on your specific situation and help identify additional strategies to mitigate your tax burden.

Remember, property taxes are determined by local jurisdictions, so it\'s essential to understand the rules specific to your area. Keep track of any changes in legislation or local ordinances that may affect property tax calculations.

READ MORE:

How does the taxpayers\' collective response to property tax increases and state revenue surplus play a role in California\'s property tax system? Remember, these questions are meant to form the basis for an in-depth article on the topic.

The taxpayers\' collective response to property tax increases and state revenue surplus has played a significant role in shaping California\'s property tax system. This response led to the passing of Proposition 13, which amended California\'s Constitution and instituted important changes to property taxation.

1. Proposition 13: In 1978, California voters approved Proposition 13 as a result of concerns over skyrocketing property tax rates. This amendment to the state Constitution imposed certain limitations on property tax increases and introduced a new system for assessing property values.

2. Limiting Property Tax Increases: Proposition 13 set a maximum limit on property tax increases at 2% per year. This means that the assessed value of a property can only increase by up to 2% each year, regardless of the actual market value appreciation. This cap provides stability and predictability for property owners by preventing sudden and drastic tax increases.

3. Assessment Method: Proposition 13 also changed the method of assessing property values. It established the concept of a \"factored base year value,\" which is the initial value established when a property is acquired and is adjusted each year by the maximum allowed 2% increase. This base year value continues to be used for property tax purposes as long as the property remains under the same ownership.

4. Property Transfers and Reassessment: Another significant aspect of Proposition 13 is that it limits reassessment of properties to specific triggering events such as a change in ownership or new construction. This means that when a property is sold or transferred, it will be reassessed at market value, and the new buyer\'s property taxes will be based on this reassessed value. However, the base year value for property tax purposes will stay the same as long as it remains under the same ownership.

5. State Revenue Surplus: The taxpayers\' response to property tax increases and the recognition of a growing state revenue surplus were influential factors in the passage of Proposition 13. The surplus indicated that there was an excess of revenue being collected by the state, which led to concerns over the fairness and affordability of property taxes. By limiting property tax increases, Proposition 13 aimed to address these concerns and provide relief to taxpayers.

Overall, the taxpayers\' collective response to property tax increases and state revenue surplus resulted in the passage of Proposition 13, which fundamentally changed California\'s property tax system. It introduced limitations on tax increases, established the concept of a factored base year value, and restricted reassessment to specific triggering events. These measures aimed to provide stability and predictability for property owners while addressing concerns over affordability and fairness in property taxation.

_HOOK_